What are the hidden costs of buying a property?

Buying a property is a big part of anyone’s life. Whether you're a

first home buyer, your third investment property, or a nice holiday house, there’s always an element of excitement involved. However, when we look at buying a property, for example, at $650,000, we often take that as how much we are paying or borrowing and don’t take into account the other hidden costs.

Unfortunately, there is no hard and fast rule on how much these hidden costs will be. It depends on how much you are paying for your property, where it’s located and whether it’s a house or part of a block of units. We’ve put together a detailed guide on all the hidden costs of buying a property that you should be including in your budget.

Conveyancing fees

First up, conveyancing fees. If you are a first home buyer, there’s a good chance that you’ve probably never heard of the word ‘conveyancer’. A conveyancer is a licensed professional who provides advice and information with regards to the transfer of property ownership, as well as organising the appropriate documents required for settlement, communicating with lenders and providing you with advice. While that might sound overwhelming, conveyancers are there to help you with the legal paperwork, and to ensure you aren’t stung with any unforeseen problems.

While it’s not required by law to have a conveyancer, it is highly recommended you do. In the short term, it might seem like it’s cheaper to do it yourself, but there is always a chance for something to go seriously wrong, which could result in disastrous consequences for you. Conveyancing prices differ from company to company; however, research indicates you can expect to pay anywhere from $1,000 - $2,500 in fees.

Stamp duty

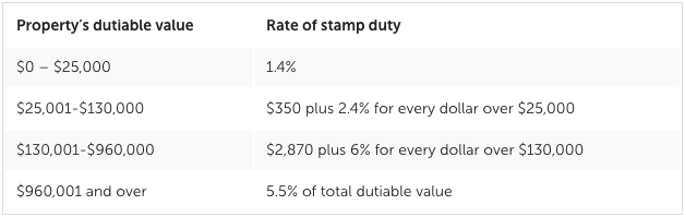

Hidden cost number two when buying a property is the big one; stamp duty. Stamp duty is the amount of tax you have to pay on any property purchase. It can be quite expensive but will vary based on how much the property is worth, where it is located and if you are a first home buyer or not. The below table from

realestate.com.au provides an example of stamp duty rates in Victoria:

For a first home buyer, however, the same stamp duty prices may not apply. The Victorian Government introduced a scheme in 2017 where first home buyers buying a house for $600,000 or less wouldn’t pay any stamp duty, and the cost of stamp duty on purchases between $600,000 - $750,000 is charged at a tapered rate.

To get an idea of how much you might have to pay in stamp duty fees, you can check our

stamp duty calculator.

Lender’s Mortgage Insurance (LMI)

According to Elliot May Lawyers, a shocking 70 per cent of borrowers in Australia believe that LMI protects them in the event of a default. This is not the case. LMI protects the lender if you cannot make your mortgage repayments.

Inovayt Senrion

Mortgage Broker Sydney, Reuben Way, explains:

“LMI is charged when the buyer has to borrow more than 80 per cent of the value of the property. LMI ranges from $1-$50,000 at the high end that is ‘capitalised’ on top of the base loan. Even though LMI is an additional cost, it helps many in this generation achieve home ownership.”

Not everyone will need to pay LMI, though. If you have a 20 per cent or higher deposit on the property you are purchasing, you will not need to pay LMI. The amount of LMI you need to pay will vary depending on how much of a deposit you are contributing to the property. However, it will also vary on several factors such as whether or not you are a first homeowner, whether you have a guarantor, whether you have genuine savings and more.

For more information, read our blogs on Lender’s Mortgage Insurance.

Building and pest inspections

While building and pest inspections aren’t compulsory, not getting one can be a serious risk with the potential for some disastrous and expensive consequences. With the hot property market we are currently seeing, houses are not meeting buyer demand and the market is moving at lightning speed. The average number of days on the market in Australia according to realestate.com.au is sitting at 48 – down from 60 in January and 71 days in June 2020. Because of this, some home buyers are bypassing this stage to save some extra money.

Reuben says: “Building and pest inspections test structural integrity and other damages like termites. Costs range from $400-$1200 depending on the size of the property. A building and pest inspection is not mandatory in Victoria, but they are in states like Queensland where most homes are built above the ground for airflow because of the hotter weather conditions. We still recommend a building and pest inspection - it is the purchaser’s responsibility to do their due diligence in buying a home. A few hundred dollars may save you hundreds of thousands in the long run.”

Although it can be tempting to cut out this cost, do so at your own risk. If there are problems with the structure of the building, or worse – like a hidden termite infestation – that an inspection could have uncovered, there is no backing out. The same thing goes for houses selling at an auction. Once the hammer has come down and the property is yours as the highest bidder, the sale is unconditional, so it’s important to arrange these inspections before the auction day.

Council and utility rates

Council and utility rates are another hidden property cost you’ll need to pay to the vendor upon purchasing the property. Rates are paid to the council – usually quarterly – which will add to the total amount of your purchase price. Rates vary from council to council, but you can generally find these fees within the Section 32.

Furniture, moving fees and repairs

If it’s your first home, you will be starting from scratch. Imagine everything in your parents’ house right now – from fridges to couches, right down to cutlery and plates. That’s a lot of stuff to get that isn’t cheap! If you do have things to take with you, you will also need to factor in the costs of moving on the day. Are you going to hire a moving van? Are you going to pay someone to help you move? These are all costs you will need to research and include.

As well as furniture, it is important to have some savings for any repairs that pop up within the first few months of buying. This could be anything from leaky taps to a busted hot water system that you hadn’t counted on when moving in.

Body corporate fees

When you’re purchasing a property in a shared facility, like a unit or apartment, you will often have to pay an annual fee which is used to cover the costs incurred within shared areas of the strata title property. These can include general maintenance and upkeep of communal areas, insurance cover, shared utilities and repairs. Your body corporate fees may be an unexpected shock if you don’t prepare and budget accordingly,

Buying a house is expensive, no matter if it’s your first or third property. But it’s the hidden costs of buying a property that often don’t get accounted for when looking for a place.

For more information on the hidden costs associated with buying a property and advice on how to include these in your budget, get in touch with one of our

mortgage broker teams today.